Keep connected

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.

Jeff Herold

April 11, 2023

In March, the preferred share market, like other risk markets, was negatively affected by bank failures in the United States and Europe, which resulted in a flight to safety bid for government bonds and a strong rally in bond markets globally. The bank crisis led to expectations of weaker future economic growth due to tighter lending standards, despite current indicators of economic activity continuing to show growth, while inflation remains well above central banks’ comfort zones. Preferred share performance was hurt by both concern about the stability of the financial sector and a federal budget proposal to eliminate the favourable tax treatment that financial institutions have on preferred share dividends. The S&P/TSX Preferred Share index ended the month with a return of -3.74%.

The U.S. bank crisis began March 8th when Silicon Valley Bank (SVB) announced a large loss on its holdings of U.S. Treasuries triggering a 25% run on its deposits in the next 24 hours. On Friday, March 10th, SVB was unable to meet withdrawal demands and the U.S. regulator, the Federal Deposit Insurance Corporation, was forced to take it over. The SVB failure triggered a flight to safety bid for government bonds that was exacerbated by another bank failure the subsequent weekend. Investors worried whether a series of bank failures would follow, and depositors at other mid-sized regional banks began shifting money to very large banks and money market funds. U.S. regulators responded by offering substantial liquidity to banks, taking their Treasury holdings at par value rather than lower market values.

The U.S. banking crisis spread to Europe as investors became concerned about the financial strength of Credit Suisse. While it appeared to have sufficient liquidity, Credit Suisse’s share price plummeted, thereby sharply reducing its apparent equity capital. As a result, the bank’s contingent convertible bonds (known as CoCo bonds) were completely written off and Credit Suisse was forced into a takeover by UBS Group. The Credit Suisse CoCos were an unusual form of Additional Tier 1 (AT1) debt because they could be completely written off if the bank’s equity fell below a required amount. In other countries, including Canada, AT1 securities are convertible into bank common shares rather than being completely wiped out if there is financial distress. Notwithstanding the differences from CoCos, Canadian bank AT1 securities, including NVCC notes, LRCNs, and preferred shares experienced sharply wider yield spreads following Credit Suisse’s collapse that was only partially unwound by month end.

Canadian economic data released in March was generally favourable. Growth in Canada’s GDP during January was faster than expected at 0.5%, and the annual increase accelerated to 3.0% from 2.3% a month earlier. The continued growth in activity suggested the Bank of Canada’s rate increases over the last year were not yet having the desired effect. In other news, unemployment remained at the low rate of 5.0%, housing starts were stronger than forecasts, and retail sales rebounded more than expected in January following weaker December results. Inflation was slightly lower than forecasts at 0.4% for the month and the annual CPI rate dropped to 5.2% from 5.9% the previous month. Wage inflation, however, accelerated to 5.4% from 4.5%. The Bank of Canada, meeting just prior to the SVB collapse, left its interest rates unchanged, as expected.

The federal budget released on March 28th contained a surprise that could impact the preferred share market. The budget proposed eliminating the favourable tax treatment that financial institutions have on the dividends received from Canadian corporations, including preferred share dividends. While banks have relatively few preferred share investments, insurance companies have for decades been major investors in preferred shares and the budget proposal may result in a reduced allocation to the asset class. The taxation change, if enacted, would likely come into effect next year.

Activity in the preferred share market was light in March. There was no new issuance of traditional $25.00 par preferred shares or institutional preferred shares during the month. On the last day of the month, Industrial Alliance completed its previously announced redemption of the $150 million IAF.PR.I series.

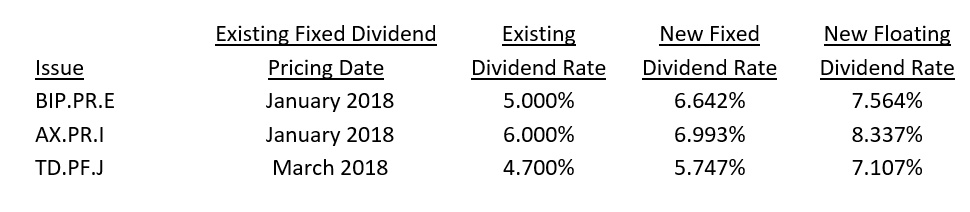

In March, there were three announcements of rate reset issue extensions. Despite the decline in bond yields during the month, the yield of the 5-year Canada bond continues to be substantially higher than five years ago, so each of the resetting issues raised their dividend rates substantially. In addition, as each issue was trading at a discount to par, the resultant increases in yields were even larger than the changes in the dividend rates. Details are as follows:

Brookfield Infrastructure subsequently announced that an insufficient number of holders of BIP.PR.E wanted to make the switch into the floating rate series, therefore all shares will be fixed rate ones, with a dividend rate of 6.642% for the next five years. Holders of AX.PR.I and TD.PF.J must make their decision on converting into the floating rate series by April 17th.

In other issuer news, at the Royal Bank April 5th annual general meeting management has proposed a change to one of the bank’s by-laws to substantially increase the maximum amount of preferred shares that the bank can issue. The proposal requires two-thirds of preferred shareholders to approve the change, however no consent fee would be paid to holders to encourage them to approve the proposal. We voted against it.

The seven largest preferred share ETFs experienced total net outflows of $76 million in March, with all but one experiencing outflows.

J. Zechner Associates Preferred Share Pooled Fund

The fund returned -1.95% in March, which was significantly better than the S&P/TSX Preferred Share index return. The sharp decline in bond yields in the month was positive for perpetual issues while rate reset issues declined as prospective dividend increases became smaller. The largest declines in rate reset share prices occurred in issues resetting in the next year. The fund benefited from having relatively few of those issues. The fund’s performance was also strengthened by its holdings of institutional preferred shares and LRCNs as those securities experienced less volatility than the traditional $25 par preferred shares that are measured by the index.

During the month, portfolio activity was limited. However, we did use some of the proceeds from the redemption of IAF.PR.I to add to the existing Bank of Montreal 7.373% institutional preferred share.

Outlook and Strategy

Despite the decline in bond yields during the month due to the flight to safety bid for government bonds, we believe that interest rates will stay higher for longer and rate reset issues will continue to benefit from sharply higher dividend rates when they reset.

As the second quarter of 2023 unfolds, we see two areas of uncertainty that are likely to dominate the attention of market participants for the next few weeks, if not months. The first is whether the banking crisis in the United States and Europe will become a rolling one, with more and more institutions succumbing to mismanagement laid bare by the rise in interest rates. If that were to happen, central banks might be forced to ease monetary policy, lowering interest rates to restore financial stability. In that event, the risk would be that inflation becomes more entrenched, making it more difficult to eradicate when central banks eventually return to their task. We are optimistic, however, that the crisis is contained and that the additional liquidity provided by the Fed and the FDIC will prove sufficient to prevent further bank failures.

The second uncertainty will be how quickly inflation returns sustainably to the 2% target rate. We anticipate that in the next few months the annual rate may fall further as very large increases in the first few months of last year are dropped from the calculation. Indeed, the annual rate of increase in CPI could fall below 4% by June. However, the pace of recent monthly increases (0.5% in January and 0.4% in February) suggests that inflation is not yet under control. Until the monthly increases shrink to roughly 0.2% and remain there, it is premature to anticipate the Bank of Canada or the Fed cutting interest rates. Some of the factors arguing against lower inflation include China’s economic reopening, the production cuts announced by OPEC+ to raise oil prices, divergent fiscal policies, and the ongoing economic strength. We expect inflation will not return sustainably to 2% for several months, which means interest rates will have to stay higher for longer than many believe.

Currently, the Canadian economy continues to grow and is not in a recession. If the banking crisis has been contained and inflation remains sticky, bond yields should reverse much, if not all, of their March rally. While growth remains positive, the need for the Bank of Canada to keep interest rates relatively high for an extended period increases the risk of a recession occurring. Despite this increased risk, we continue to remain confident in the creditworthiness of the issuers in the portfolio. The fund’s average yield of 6.47%, much of it due to tax advantaged dividends, seems attractive.

Our investment management team is made up of engaged thought leaders. Get their latest commentary and stay informed of their frequent media interviews, all delivered to your inbox.